Over the past decade large numbers of UK residents and expatriates have chosen to move their pensions into Qualifying Recognised Overseas Pension Schemes (QROPS). While some did so to align their retirement savings with life abroad, others are now looking to bring their pensions back to the UK. In many cases the return is driven by relocation, but for some the shift from perceived flexibility to regulatory complexity has prompted a rethink.

Several overseas schemes have since been removed from HMRC’s official QROPS list, meaning they no longer meet the criteria to be recognised as QROPS. This delisting has serious consequences, including frozen access to funds, restrictions on transfers and significant uncertainty around long-term retirement planning. If your QROPS was once legitimate but is now de-listed, you may be wondering whether you can transfer your pension back to the UK or elsewhere or whether you are effectively trapped.

What Happens When a QROPS is Delisted?

It is important to emphasise that the delisting of a scheme does not invalidate the original transfer if it took place while the scheme was properly recognised by HMRC. However, once a scheme loses its QROPS status, any future transfers from that scheme might not benefit from UK tax protections. Some providers, concerned about regulatory risk, may freeze access or block transfers altogether. Attempting to move your pension funds under these conditions can create additional reporting obligations and tax risks, leaving expatriates in a difficult position.

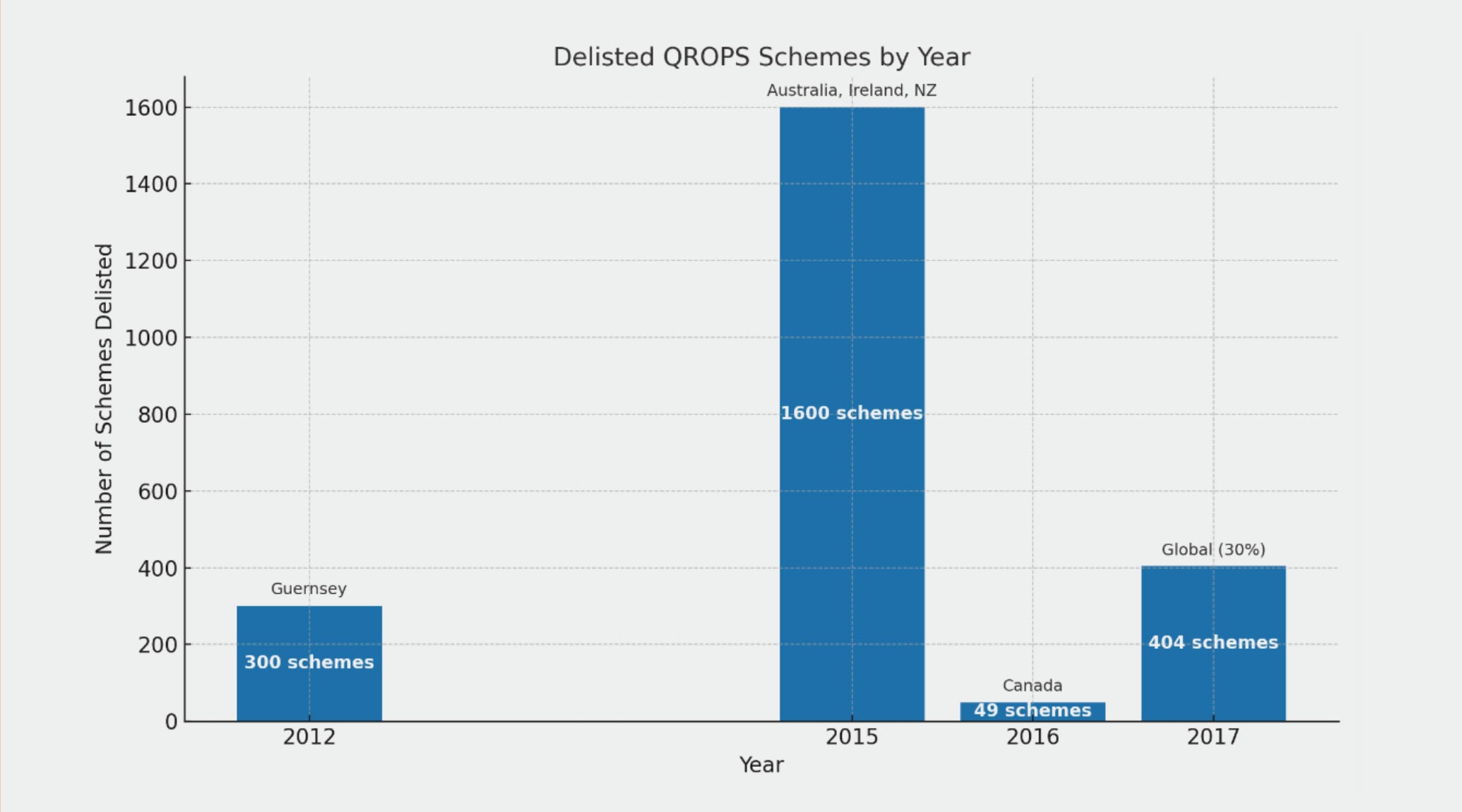

Delisted QROPS: A Global Shift

Between 2012 and 2017, HMRC removed hundreds of QROPS from its recognised list, impacting entire jurisdictions. Guernsey lost over 300 schemes in 2012 alone. In 2015, Australia dropped from 1,600 schemes to just one, with Ireland and New Zealand similarly affected

HMRC’s Guidance Offers a Route Forward

There is some positive news amid this uncertainty. HMRC has clarified in its Pensions Tax Manual (PTM100010) that registered UK pension schemes may accept transfers from any type of pension scheme. This includes not only other registered UK schemes but also qualifying recognised overseas pension schemes, even if those schemes are no longer recognised as QROPS and other non-UK pension arrangements.

Further clarity comes from HMRC’s guidance in PTM103500, which explains that a transfer from a QROPS or former QROPS to a UK-registered pension scheme is not treated as a new contribution but rather as the relocating of existing pension rights. This distinction can provide peace of mind for expatriates concerned about unintended tax consequences when moving their funds back into UK-registered schemes such as SIPPs.

While these HMRC positions do not guarantee every scheme or provider will accept transfers from de-listed QROPS, they do confirm that UK pension schemes have the regulatory framework to facilitate such transfers, provided all due diligence and compliance requirements are met.

What Should You Do If You Are Affected

If your pension is in a de-listed QROPS, it is critical to carefully assess your current scheme’s status and what options are available to you. Check whether your provider allows transfers out and understand the tax rules in your country of residence, as local authorities may treat transfers differently from the UK.

Given the complexity of cross-border pensions, it is essential to seek advice from a regulated financial professional experienced in international pension transfers. They can help you evaluate whether a transfer back to a UK-registered scheme is appropriate in your circumstances and guide you through any potential tax implications.

Avoid making hasty decisions. Acting without full clarity could lead to unexpected tax liabilities or restrictions that may affect your retirement income and legacy plans.

You Are Not Alone

Overseas pension rules shift frequently, and many UK residents (and returning expats) only discover the pitfalls years after transferring. However, with the right advice and support, you can explore your options confidently and work towards a compliant and sustainable retirement outcome.

Get Clear. Get Options. Get Peace of Mind.

If you hold a QROPS and are uncertain of your options, our regulated advisers are here to help.

We offer a confidential review of your pension arrangements and will assess whether transferring back to a UK-registered pension scheme is a suitable and viable option for you.

Our experts will guide you through the complex rules and tax implications in both the UK and your country of residence, helping you make informed decisions with confidence.

Contact us today to arrange your no-obligation consultation and take the first step towards securing your retirement.

FCA regulated | Experienced cross-border pension specialists

Important Notice

Suitability of any pension transfer or tax mitigation strategy depends on individual circumstances. Please seek regulated advice before making any decisions.